Bankster's Holiday 2 - Our Economy Down The Drain

Government incompetence and cupidity caused the financial crash.

-

Tools:

The first article in this series explained how government regulation generally fails to cure problems for which it is set up. What's worse, government meddling in the housing market first inflated the housing bubble and then popped it, leading to the Obama depression. A serious problem with government meddling is that the dire results can take a long time to manifest themselves, but when the collapse comes, they're unstoppably awful. When government meddles, it meddles on a massive scale which leads to massive disasters.

When the financial crash took place in 2008, the consequences were far worse than the regulators had ever dreamed possible. Lehman's collapse put such a scare into every investor, banker, and financier that it seemed like our national banking system might seize up entirely.

Every single aspect of our modern financial networks other than cold hard cash in a suitcase, drug-dealer style, depends on trust. When you receive a check, you trust that the bank whose name is on it will honor the check and give you the money. When you use a credit card, the merchant trusts that your bank will eventually give them the money. When banks receive wire-transfers and other financial instruments, they trust that the money will be there when it's all reconciled at the end of the month.

When Lehman, one of the world's largest financial firms, unexpectedly evaporated over a weekend, nobody seemed safe. Who can you trust? The wisest answer for one individual person or firm is "trust nobody," but when everyone reaches that conclusion at the same time, our entire monetary system disappears with a pop and our economy instantly collapses because nothing that requires exchanging money can function.

The government decided that it, the government, was the only entity large enough to be trusted, and that therefore it had to guarantee all the banks in order to keep them functioning. To this end, the Treasury and Federal Reserve made billions and billions of dollars worth of TARP and other loans, basically in whatever amounts and to whatever recipients seemed like a good idea at the time.

Mortgage Relief, Without the Relief

Since the Democrats had spent years justifying Fannie and Freddie as necessary to put people who couldn't meet normal credit standards in homes of their own, they naturally wanted to do something to keep all those people from losing their homes. This proved very difficult, however. Federal "mortgage relief" programs were unable to make a significant dent in the number of people who were at risk of losing their homes. The reason was simple - these "owners" weren't really able to make payments in the good times, never mind once the recession started and many of them lost their jobs.

The legislation that allowed the government to spend billions propping up the banks required the banks to do their best to recover the assets and convert themselves back to profitability. Taxpayers were screaming bloody murder about the TARP billions; the government had to get at least some of its money back or heads would roll. The only way to get the money back would be for the banks to become profitable again.

When a "homeowner" wasn't paying the mortgage, the only way to get money to reduce the outstanding loan was foreclosing on the property and trying to sell it off. Although the bank would get less for the house than it had loaned, there'd be at least some cash, and the dud loan would be off the books. Cleaning up the books would let the bank get back to business as usual.

What's more, it's only right that anyone who obtained a home fraudulently or who simply decided to stop paying on a loan in order to enjoy free rent for a while should be thrown out of the house as rapidly as possible. As angry as voters were that billionaire banks got taxpayer help, if enough ordinary people got houses for free courtesy of Uncle Sap there'd be civil war.

Thus, it was no surprise that, once bankers' heads stopped spinning, banks started to foreclose in earnest.

|

| Foreclosure in progress. |

The Foreclosure Fraud Fiasco

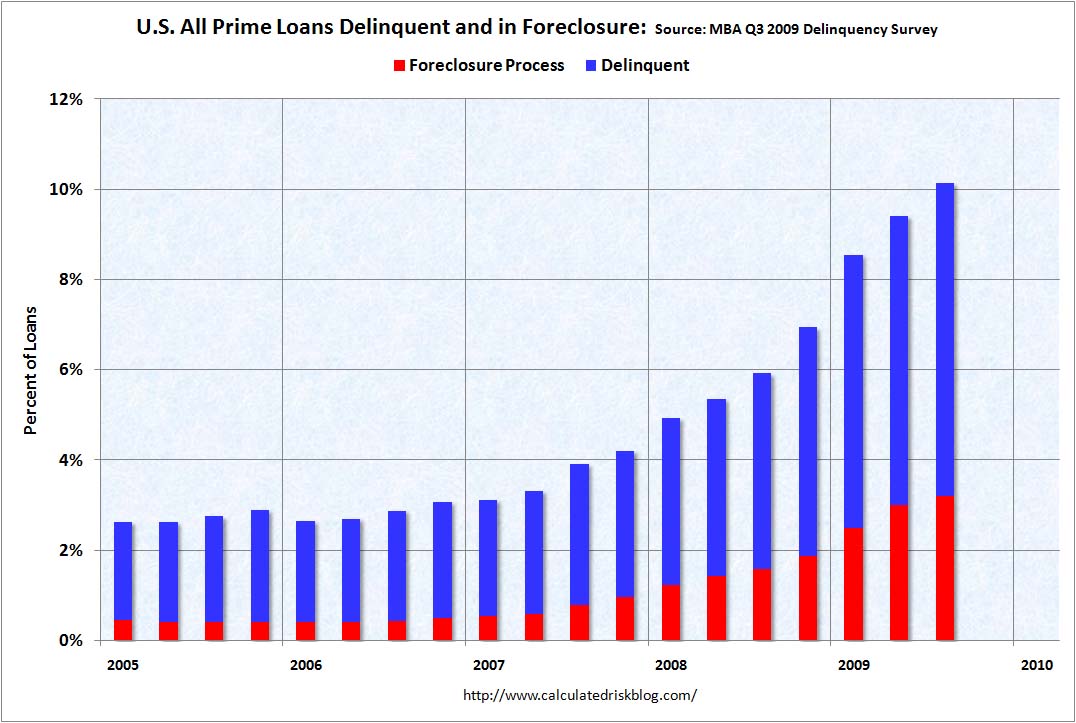

The problem was that foreclosure volume exploded as the banks tried to clean up the mess. A system designed for around 2% of loans being troubled was suddenly called upon to process five times as many.

{kind=link}

Since losing a home is pretty traumatic for the homeowner, most states have fairly stringent regulations in place to prevent casual foreclosure. The banks have to present papers showing:

- That the bank actually owns the loan and is therefore legally entitled to ask the court to declare the homeowner to be in default. When the court takes the home away from the owner, it has to be given to someone, and the bank needs to satisfy the court that the bank should be given clear title to the house.

- That the bank has verified to the penny precisely how much the homeowner owes on the loan. When the home finally sells, the homeowner gets a check for any additional money gotten over and above the debt - which is only fair, it was their house - so the bank has to tell the court how much the bank plans to deduct from the selling price. Most foreclosures these days are underwater so there wouldn't be any extra, but it's still the rule.

- A certification that the bank employees or agents have checked all the papers thoroughly and are prepared to swear that everything is being done accurately and according to due process. The courts don't want to employ skilled bankers to actually understand all the documents, so they extend some trust to the banks, but if the bankers lie it's perjury.

This is a pretty complex and exacting procedure, as well it should be. There's no public purpose to be served in making it too easy to throw people out of their homes. The complexities of foreclosure are a set of regulations which ought, in theory, to protect people against wrongful foreclosure.

There were problems.

The mortgages had been sold and re-sold so many times that it wasn't always clear who owned any particular mortgage. Some banks had placed ownership of the mortgages with a third party and sold the right to collect income from the mortgages instead of selling the mortgages themselves. In these cases, ownership was clear, but when the mortgages had been sold without filling out the required transfer forms and paying state-imposed transfer taxes, ownership of the mortgage was difficult to establish. Scragged wrote about this part of the foreclosure problem some time ago.

Even when mortgage ownership, as opposed to the right to collect payments on the mortgage, was well established, the sheer volume of paperwork made it difficult to cross all the t's and dot all the i's as the law demands. Foreclosure had been a relatively sleepy corner of the banking business because foreclosures were rare.

Now that the government had induced banks to lend to so many people who couldn't pay, however, volume doubled in a year, then doubled again the next year. This overwhelmed the courts - processing a foreclosure averages 478 days, up from 302 days in early 2005. The volume also swamped all the foreclosure departments in every bank and in all the outside mortgage service providers. Many new people were hired to process mortgages and quality went down. As the New York Times put it,

At JPMorgan Chase & Company, they were derided as "Burger King kids" - walk-in hires who were so inexperienced they barely knew what a mortgage was.

At Citigroup and GMAC, dotting the i's and crossing the t's on home foreclosures was outsourced to frazzled workers who sometimes tossed the paperwork into the garbage.

And at Litton Loan Servicing, an arm of Goldman Sachs, employees processed foreclosure documents so quickly that they barely had time to see what they were signing.

"I don't know the ins and outs of the loan," a Litton employee said in a deposition last year. "I'm not a loan officer." [emphasis added]

The statement by the Litton employee is particularly telling - most state laws require that the specific person who signed off on the documents be prepared to swear that the documents were factually correct and accurate. That requires that the person who signs the papers read them, understand them, and verify that the numbers are right. If you have no clue what a proper mortgage is supposed to look like, doing this honestly is patently impossible.

Deliberately presenting court papers which do not meet legally-required standards is a crime. It's an even more serious crime if the banks knowingly present inadequate papers and swear that they've been prepared correctly. Thus, banks seem to have engaged in wholesale criminal activity in trying to clean up the mortgage mess.

This isn't just a case of greedy businessmen trying to exploit needy homeowners, as bad as that would be. In "Foreclosure fiasco trail leads to Washington," Bloomberg News reports:

What were banking regulators doing while some of the biggest U.S. lenders routinely filed false foreclosure documents in local courthouses around the country? In the case of IndyMac Federal Bank, it turns out the Federal Deposit Insurance Corp. was running the joint.

This may help explain why the mortgage-servicing industry got away with such misbehavior for so long. The government, in one form or another, was doing it, too.

The facts are there for anyone to see in the records of a Florida circuit court lawsuit against Israel and Neena Machado, a West Palm Beach couple who last year beat back IndyMac's attempts to foreclose on their home mortgage. They even won a judgment ordering IndyMac to pay $38,117 in legal fees. [emphasis added]

The Indy Mac bank failed in 2008 and was taken over by the FDIC, which is required to operate a failed bank until it can be sold. While the government was running the bank, an IndyMac vice president, Erica Johnson-Seck, swore that she had personal knowledge of the money the Machados owed the bank. That simply wasn't true; she lied to the court as she later admitted.

The banking regulators let the banks commit widespread fraud. At IndyMac, though, the FDIC wasn't just regulating the bank, it was running the bank while the bank committed mass fraud.

This is precisely the sort of situation regulators are supposed to prevent, yet the government failed utterly in this duty, even at a bank that was operating under direct government control. Once again, the agencies which failed in their duty are being rewarded with bigger budgets under the new financial reorganization act. We expect bigger and messier failures now that they have so much more money to fund bigger and messier failures.

-

Tools:

What does Chinese history have to teach America that Mr. Trump's cabinet doesn't know?